Investment Intelligence: Q1 Active Deal Pipeline

In the fast-paced investment world, staying ahead of the curve is crucial. Earlier this year, we pulled back the curtain on our data-driven deal analysis by publishing a look at our 2023 Active Deal Pipeline. As we look back at 2024 to date, we continue to discover, evaluate, and track potential deals in search of investment opportunities for our firm and our clients. This updated dashboard reveals key data points and trends based on the 79 deals our analysts reviewed in 2024.

What Deals Make the List?

Our Active Deal Pipeline consists of deals sourced by DCA in 2024 that led to deeper due diligence by our investment team. As a firm, DCA invests in high-growth-potential startups, with a focus on tech businesses that have the potential to disrupt established industries. Many of our portfolio companies transcend industry lines. Thus, while we remain agnostic to industries and geographies, we highlight some of the more attractive verticals in which our attention and investment dollars are concentrated.

A High-Level Look at Q1 2024

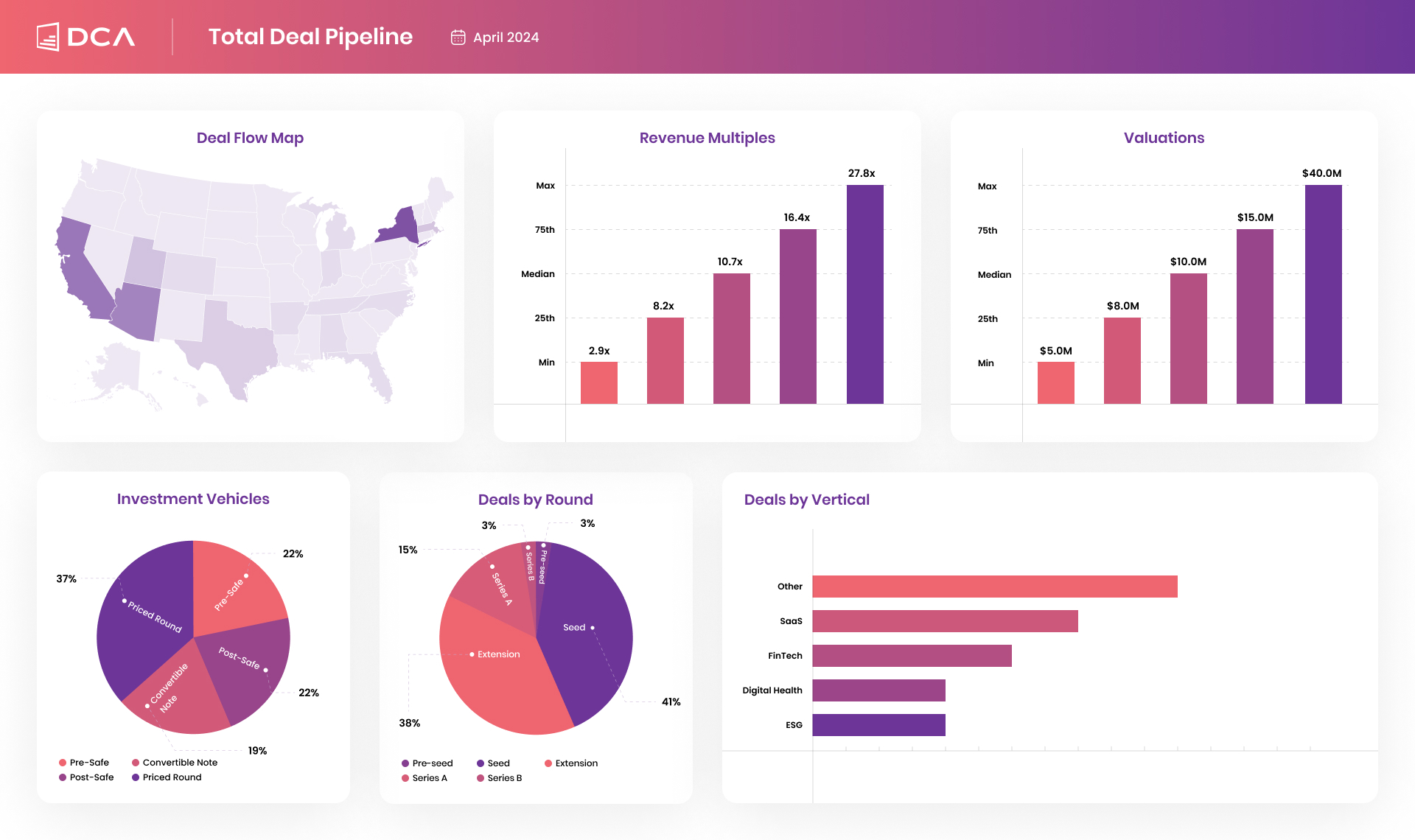

Our Active Deal Pipeline presents a dashboard view of the 79 deals that fit our investment model since January of 2024, organized by geography, vertical, investment vehicle, round, revenue multiples, and valuations. As a firm, DCA Asset Management has meticulously sourced and reviewed hundreds of deals in Q1’24. Our current pipeline consists of 79 early-stage deals, of which 17 are actively undergoing diligence, while the other 62 are in the initial stages of assessment.

What follows are takeaways from our deal analysis as of April 2024:

Investment Vehicles: Convertible Debt and Priced Rounds

Among the 79 deals in our pipeline, a significant majority (63%) are being raised on convertible debt vehicles. Specifically, 44% of the deals utilize Simple Agreements for Future Equity (SAFEs), while 19% rely on Convertible Notes. This reflects the prevailing trend of extension rounds in the early-stage market, allowing startups to extend previous round runways and capitalize on key performance indicators. Notably, 37% of the deals in the pipeline involve traditional priced rounds.

Geography: Diverse Deal Concentration

Our current pipeline deals span across 18 states, with notable concentrations in New York (12 deals), California (9 deals), and Arizona (8 deals). However, DCA Asset Management maintains a geography-agnostic investment strategy, with the rest of the pipeline deals evenly distributed across the Mountain West, Midwest, and East Coast.

Funding Stage: Seed and Seed Extensions Dominate

The majority of deals in our pipeline (79%) fall within the Seed and Seed Extension investment stages. This highlights the prevalence of early-stage investments and the increasing need for additional funding to fuel growth in promising startups. Series A deals represent 15% of the active deal pipeline.

Verticals: Tech-focused Sectors Lead the Way

Verticals SaaS (24%) and Fintech (18%) emerge as the most prominent verticals within our active deal pipeline. These sectors demonstrate significant potential for growth, innovation, and disruption. Digital Health (12%) and ESG (12%) also feature prominently, indicating promising opportunities in these markets.

Valuation: Ranging from $5M to $40M

Our 79 active deals in the pipeline exhibit varying valuations, with a current range of $5 million (Pre-seed EdTech deal) to $40 million (Series A FinTech deal). The median valuation for deals in our pipeline stands at $10 million, reflecting the diverse range of opportunities we evaluate.

Data-Driven Deal Analysis

At DCA Asset Management, we are dedicated to leveraging data-driven strategies to inform our investment decisions. As our Active Deal Pipeline continues to evolve, we remain committed to staying at the forefront of the investment landscape to help our clients thrive in an ever-changing market.

—

*One of DCA’s guiding principles is that we will communicate with our investors and prospective investors as candidly as possible because we believe investors and prospective investors benefit from understanding our investment philosophy and approach. Our views and opinions regarding the prospects of investments and/or the economy are forward looking statements as defined under the U.S. federal securities laws, which may or may not be accurate and may be materially different over future periods. Generally, the words “believe,” “expect,” “intend,” “estimate,” “anticipate,” “project,” “will,” “may,” “should,” “plan,” or the negative of such terms and similar expressions identify forward looking statements. Forward looking statements are subject to certain risks and uncertainties that could cause actual results to materially differ from an investor’s historical experience and current expectations or projections indicated in any forward looking statements. These risks include, but are not limited to, equity securities risk, corporate bonds risk, credit risk, interest rate risk, leverage and borrowing risk, additional risks of certain investments, management risk, and other risks. We disclaim any obligation to update or alter any forward looking statements, whether as a result of new information, future events, or otherwise. You should not place undue reliance on forward looking statements, which speak only as of the date they are made.